Obesity Market Size, Epidemiology, In-Market Drugs Sales: Market Overview

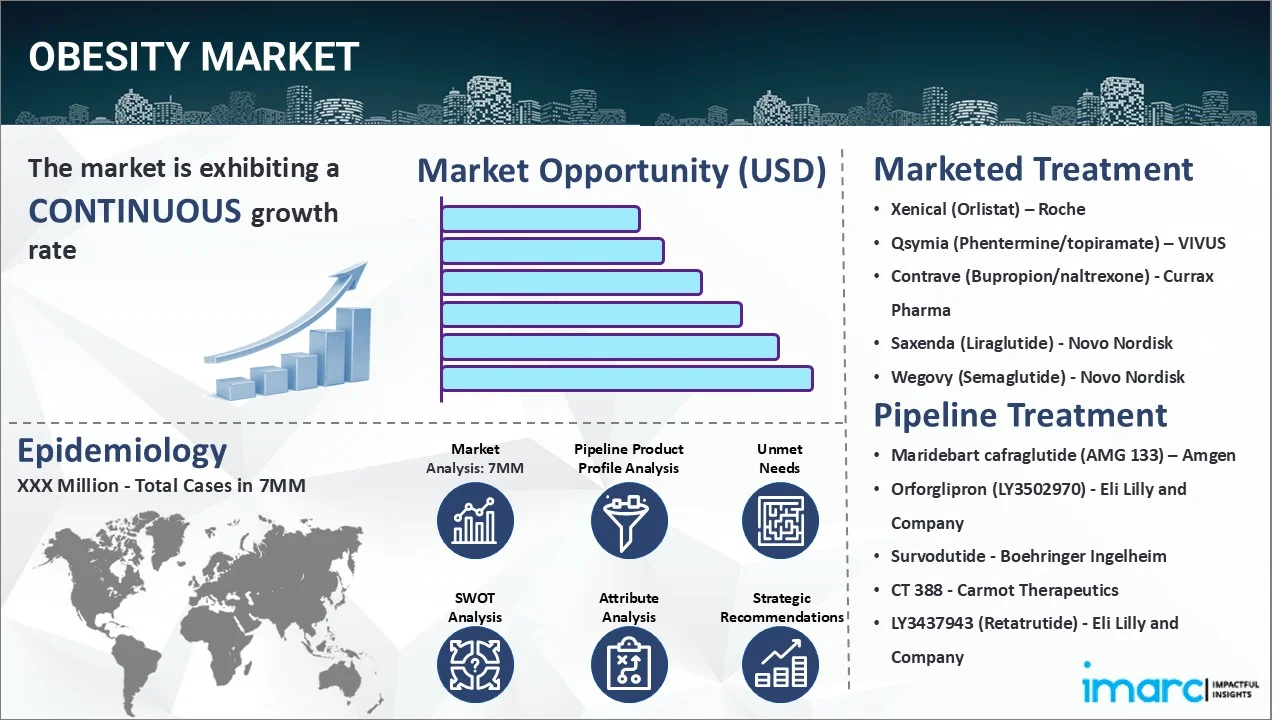

The 7 major obesity markets reached a value of USD 6.5 Billion in 2023. Looking forward, the 7MM are expected to reach USD 135.8 Billion by 2036, exhibiting a growth rate (CAGR) of 28.5% during 2024-2036.

Report Attribute | Key Statistics |

| Base Year | 2023 |

| Forecast Period | 2024-2036 |

| Historical Period | 2018-2023 |

Market Size in 2023 | USD 6.5 Billion |

Market Forecast in 2036 | USD 135.8 Billion |

Market Growth Rate (CAGR) | 28.5% |

The obesity market has been comprehensively analyzed in this new report titled "Obesity Market Size, Epidemiology, In-Market Drugs Sales, Pipeline Therapies, and Regional Outlook 2024-2036". Obesity is a complex, chronic disease characterized by excessive body fat accumulation that presents a risk to health. The World Health Organization (WHO) defines overweight and obesity as having a Body Mass Index (BMI) of 25 or greater and 30 or greater, respectively. This condition significantly increases the risk of numerous comorbidities, including type 2 diabetes, cardiovascular diseases, hypertension, certain cancers, and musculoskeletal disorders. Diagnosis involves calculating BMI, measuring waist circumference, and assessing for the presence of obesity-related health problems. Blood tests may also be conducted to check cholesterol, blood sugar, and liver function to evaluate the overall metabolic health of the patient.

The primary driver for the obesity market is the dramatic increase in the global prevalence of the condition, fueled by sedentary lifestyles, and the widespread availability of high-calorie foods. A significant catalyst for market growth is the recent introduction and rapid uptake of highly effective anti-obesity medications (AOMs), particularly GLP-1 receptor agonists like semaglutide and tirzepatide. These drugs have demonstrated unprecedented weight loss efficacy, transforming the treatment landscape and driving substantial market expansion. Furthermore, a growing understanding of obesity as a chronic disease, rather than a lifestyle choice, is reducing stigma and encouraging more individuals to seek medical treatment. This shift is supported by expanding reimbursement coverage for AOMs and bariatric surgery in several key markets. The robust pipeline of next-generation therapies, including dual and triple agonists (e.g., retatrutide) and oral formulations, promises even greater efficacy and convenience, which is expected to sustain strong market growth throughout the forecast period.

This report provides an exhaustive analysis of the obesity market in the United States, EU5 (Germany, Spain, Italy, France, and United Kingdom) and Japan. This includes treatment practices, in-market, and pipeline drugs, share of individual therapies, market performance across the seven major markets, market performance of key companies and their drugs, etc. The report also provides the current and future patient pool across the seven major markets. According to the report the United States has the largest patient pool for obesity and also represents the largest market for its treatment. Furthermore, the current treatment practice/algorithm, market drivers, challenges, opportunities, reimbursement scenario and unmet medical needs, etc. have also been provided in the report. This report is a must-read for manufacturers, investors, business strategists, researchers, consultants, and all those who have any kind of stake or are planning to foray into the obesity market in any manner.

Recent Developments:

In February 2025, Eli Lilly and Company announced positive top-line results from its SURMOUNT-5 Phase 3 clinical trial evaluating retatrutide (a GIP/GLP-1/glucagon receptor tri-agonist) in adults with obesity. The study met its primary endpoints, showing a mean weight reduction of over 25% at 72 weeks, setting a new benchmark for pharmacological weight loss therapies and reinforcing the company's leadership in the metabolic space.

In December 2024, Novo Nordisk received FDA approval for an oral formulation of semaglutide for chronic weight management. The approval of this new, more convenient dosage form is expected to significantly expand patient access and further accelerate the growth of the Wegovy franchise by catering to patients with an aversion to injections.

In November 2024, Pfizer Inc. reported disappointing results from a Phase 2b study of its oral GLP-1 receptor agonist, danuglipron, citing high rates of gastrointestinal side effects. The company announced it would discontinue the twice-daily formulation and focus on developing a once-daily, modified-release version to improve tolerability and remain competitive in the crowded oral obesity drug market.

Drugs:

Wegovy (Semaglutide) is an injectable glucagon-like peptide-1 (GLP-1) receptor agonist developed by Novo Nordisk. It is administered once-weekly and works by mimicking the GLP-1 hormone, which targets areas of the brain that regulate appetite and food intake. This leads to reduced hunger, increased feelings of fullness, and consequently, lower calorie consumption and significant weight loss. It is also approved to reduce the risk of major adverse cardiovascular events in adults with established cardiovascular disease and either obesity or overweight.

Zepbound (Tirzepatide), from Eli Lilly and Company, is a once-weekly injectable dual glucose-dependent insulinotropic polypeptide (GIP) and GLP-1 receptor agonist. By activating both GIP and GLP-1 pathways, Zepbound provides a synergistic effect on appetite regulation, energy expenditure, and glucose control, leading to substantial weight loss that has been shown in clinical trials to be superior to that of GLP-1 agonists alone.

Retatrutide (LY3437943) is an investigational triple-hormone-receptor agonist being developed by Eli Lilly and Company. It targets the GIP, GLP-1, and glucagon receptors. This multi-agonist approach is designed to further enhance weight loss by not only suppressing appetite and improving insulin sensitivity (via GIP/GLP-1) but also by increasing energy expenditure (via glucagon). Early-phase trials have shown unprecedented levels of weight reduction, positioning it as a potential next-generation leader in obesity treatment.

Time Period of the Study

Base Year: 2023

Historical Period: 2018-2023

Market Forecast: 2024-2036

Countries Covered

United States

Germany

France

United Kingdom

Italy

Spain

Japan

Analysis Covered Across Each Country

Historical, current, and future epidemiology scenario

Historical, current, and future performance of the obesity market

Historical, current, and future performance of various therapeutic categories in the market

Sales of various drugs across the obesity market

Reimbursement scenario in the market

In-market and pipeline drugs

Competitive Landscape:

This report also provides a detailed analysis of the current obesity marketed drugs and late-stage pipeline drugs.

In-Market Drugs

Drug Overview

Mechanism of Action

Regulatory Status

Clinical Trial Results

Drug Uptake and Market Performance

Late-Stage Pipeline Drugs

Drug Overview

Mechanism of Action

Regulatory Status

Clinical Trial Results

Drug Uptake and Market Performance

| Drugs | Company Name |

| Wegovy (Semaglutide) | Novo Nordisk |

| Zepbound (Tirzepatide) | Eli Lilly and Company |

| Saxenda (Liraglutide) | Novo Nordisk |

| Qsymia (Phentermine/topiramate) | VIVUS |

| Contrave (Bupropion/naltrexone) | Currax Pharma |

| Retatrutide (LY3437943) | Eli Lilly and Company |

| Maridebart cafraglutide (AMG 133) | Amgen |

| Survodutide (BI 456906) | Boehringer Ingelheim/Zealand Pharma |

| CagriSema (semaglutide/cagrilintide) | Novo Nordisk |

| Orforglipron (LY3502970) | Eli Lilly and Company |

*Kindly note that the drugs in the above table only represent a partial list of marketed/pipeline drugs, and the complete list has been provided in the report.

Key Questions Answered in this Report:

Market Insights

How has the obesity market performed so far and how will it perform in the coming years?

What are the markets shares of various therapeutic segments in 2023 and how are they expected to perform till 2036?

What was the country-wise size of the obesity market across the seven major markets in 2023 and what will it look like in 2036?

What is the growth rate of the obesity market across the seven major markets and what will be the expected growth over the next twelve years?

What are the key unmet needs in the market?

Epidemiology Insights

What is the number of prevalent cases (2018-2036) of obesity across the seven major markets?

What is the number of prevalent cases (2018-2036) of obesity by age across the seven major markets?

What is the number of prevalent cases (2018-2036) of obesity by gender across the seven major markets?

How many patients are diagnosed (2018-2036) with obesity across the seven major markets?

What is the size of the obesity patient pool (2018-2023) across the seven major markets?

What would be the forecasted patient pool (2024-2036) across the seven major markets?

What are the key factors driving the epidemiological trend of obesity?

What will be the growth rate of patients across the seven major markets?

Obesity: Current Treatment Scenario, Marketed Drugs and Emerging Therapies

What are the current marketed drugs and what are their market performance?

What are the key pipeline drugs and how are they expected to perform in the coming years?

How safe are the current marketed drugs and what are their efficacies?

How safe are the late-stage pipeline drugs and what are their efficacies?

What are the current treatment guidelines for obesity drugs across the seven major markets?

Who are the key companies in the market and what are their market shares?

What are the key mergers and acquisitions, licensing activities, collaborations, etc. related to the obesity market?

What are the key regulatory events related to the obesity market?

What is the structure of clinical trial landscape by status related to the obesity market?

What is the structure of clinical trial landscape by phase related to the obesity market?

What is the structure of clinical trial landscape by route of administration related to the obesity market?