Obesity Market Size and Share Analysis

Market Overview:

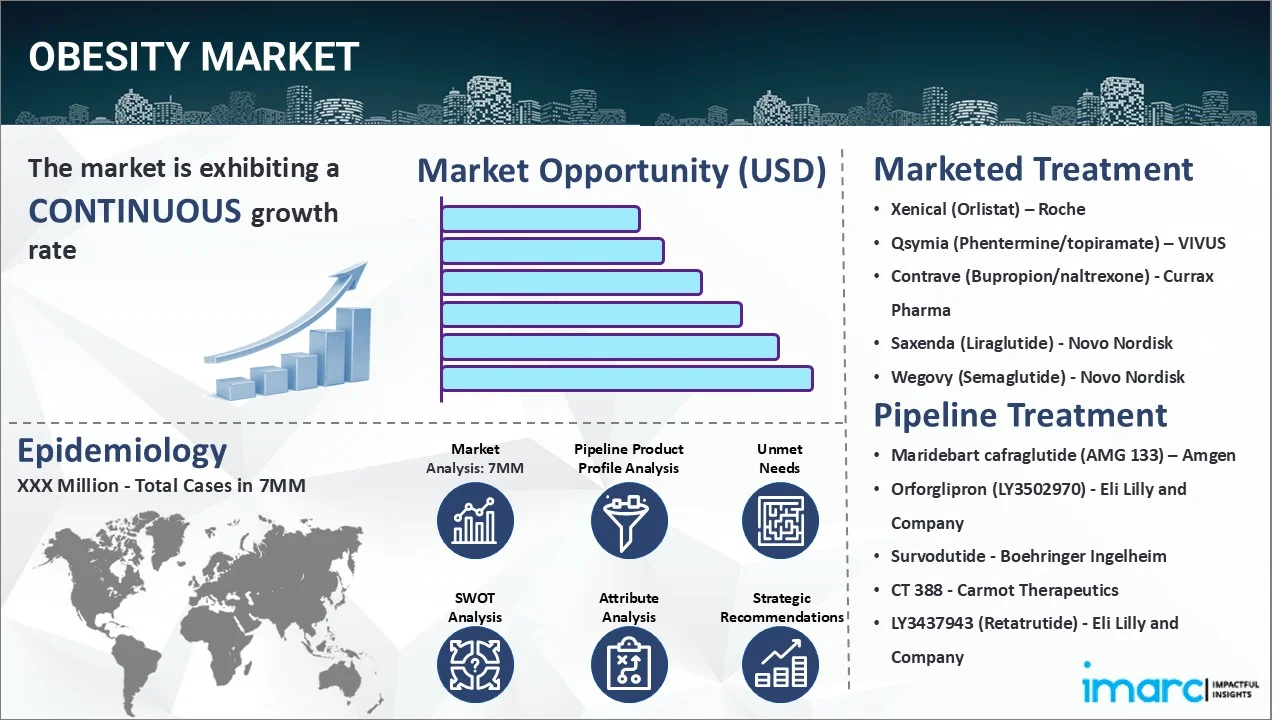

The 7 major obesity markets reached a value of USD 35.8 Billion in 2024. Looking forward, IMARC Group expects the 7MM to reach USD 120.5 Billion by 2035, exhibiting a growth rate (CAGR) of 12.21% during 2025-2035. The United States represents the largest market share, driven by a high prevalence rate and the strong uptake of novel therapeutics.

|

Report Attribute

|

Key Statistics

|

|---|---|

| Base Year | 2024 |

| Forecast Years | 2025-2035 |

| Historical Years |

2019-2024

|

|

Market Size in 2024

|

USD 35.8 Billion |

|

Market Forecast in 2035

|

USD 120.5 Billion |

|

Market Growth Rate 2025-2035

|

12.21% |

The obesity market has been comprehensively analyzed in IMARC's new report titled "Obesity Market Size, Epidemiology, In-Market Drugs Sales, Pipeline Therapies, and Regional Outlook 2025-2035". Obesity is a complex, chronic disease characterized by excessive body fat accumulation that presents a risk to health. The World Health Organization (WHO) defines an adult as obese if their body mass index (BMI), a measure of weight-for-height, is 30 or higher. The condition significantly increases the risk of numerous comorbidities, including type 2 diabetes, cardiovascular diseases (like heart attack and stroke), hypertension, certain types of cancer, and musculoskeletal disorders. Diagnosis primarily involves calculating the BMI, though other methods like measuring waist circumference, assessing skinfold thickness, and bioelectrical impedance analysis are also used. Healthcare providers conduct a thorough physical examination and review the patient's medical and family history, along with lifestyle factors such as diet and physical activity, to form a complete diagnosis and treatment plan.

The primary driver for the obesity market is the escalating global prevalence of the condition, fueled by sedentary lifestyles, changing dietary patterns towards high-calorie processed foods, and genetic predispositions. In addition to this, a significant market driver is the recent paradigm shift in viewing obesity as a chronic disease rather than a lifestyle choice, which has increased both patient willingness to seek treatment and physician proactivity in prescribing it. This has been supported by the groundbreaking launch of highly effective anti-obesity medications (AOMs), such as GLP-1 receptor agonists like semaglutide and tirzepatide, which have demonstrated unprecedented weight loss results, thereby boosting market growth. Furthermore, growing public awareness of the severe health complications associated with obesity is encouraging more individuals to seek medical intervention. The market is also bolstered by expanding reimbursement coverage for AOMs and bariatric surgery in several countries, making treatments more accessible. Technological advancements in minimally invasive bariatric procedures and a robust pipeline of next-generation therapies with improved efficacy and safety profiles are expected to drive the obesity market significantly during the forecast period.

IMARC Group's new report provides an exhaustive analysis of the obesity market in the United States, EU5 (Germany, Spain, Italy, France, and United Kingdom) and Japan. This includes treatment practices, in-market, and pipeline drugs, share of individual therapies, market performance across the seven major markets, market performance of key companies and their drugs, etc. The report also provides the current and future patient pool across the seven major markets. According to the report the United States has the largest patient pool for obesity and also represents the largest market for its treatment. Furthermore, the current treatment practice/algorithm, market drivers, challenges, opportunities, reimbursement scenario and unmet medical needs, etc. have also been provided in the report. This report is a must-read for manufacturers, investors, business strategists, researchers, consultants, and all those who have any kind of stake or are planning to foray into the obesity market in any manner.

Recent Developments:

In March 2025, Eli Lilly and Company announced that the U.S. Food and Drug Administration (FDA) had granted a supplemental New Drug Application (sNDA) for Zepbound (tirzepatide) to reduce the risk of major adverse cardiovascular events (MACE) in adults with obesity or overweight with established cardiovascular disease. This approval significantly expands the drug's label and reinforces its clinical value beyond weight management.

In January 2025, Amgen reported positive top-line results from its pivotal Phase 3 study of MariTide (maridebart cafraglutide), an investigational bispecific molecule. The study met its primary endpoints, demonstrating statistically significant and clinically meaningful weight loss compared to placebo in adults with obesity. The company plans to file for regulatory approval in the U.S. and Europe by the end of the year.

In December 2024, Novo Nordisk A/S revealed plans to invest over $2 billion to expand its manufacturing facilities in North America to meet the surging demand for its GLP-1-based therapies, Wegovy (semaglutide) and Ozempic. This strategic investment aims to alleviate supply constraints and ensure broader patient access to its leading obesity and diabetes treatments.

Drugs:

Wegovy (Semaglutide), developed by Novo Nordisk, is a glucagon-like peptide-1 (GLP-1) receptor agonist administered as a once-weekly subcutaneous injection. It mimics the effects of the natural GLP-1 hormone by targeting areas of the brain that regulate appetite and food intake. This leads to reduced hunger, increased feelings of fullness, and consequently, lower calorie consumption and significant weight loss. It is indicated for chronic weight management in adults with obesity or overweight with at least one weight-related comorbidity.

Zepbound (Tirzepatide) is an injectable prescription medicine from Eli Lilly and Company for adults with obesity. It is the first and only approved treatment that activates two different hormone receptors, GIP (glucose-dependent insulinotropic polypeptide) and GLP-1. This dual-action mechanism is believed to contribute to its superior weight loss effects by regulating appetite, food intake, and metabolic function more comprehensively than single-agonist therapies.

Retatrutide (LY3437943), an investigational therapy from Eli Lilly and Company, is a triple-agonist receptor agonist targeting GLP-1, GIP, and glucagon receptors. This multi-faceted approach aims to leverage the combined metabolic benefits of all three gut hormones to achieve even greater reductions in weight and improvements in metabolic health, including fat and glucose metabolism. It is currently in late-stage clinical development.

Time Period of the Study

- Base Year: 2024

- Historical Period: 2019-2024

- Market Forecast: 2025-2035

Countries Covered

- United States

- Germany

- France

- United Kingdom

- Italy

- Spain

- Japan

Analysis Covered Across Each Country

- Historical, current, and future epidemiology scenario

- Historical, current, and future performance of the obesity market

- Historical, current, and future performance of various therapeutic categories in the market

- Sales of various drugs across the obesity market

- Reimbursement scenario in the market

- In-market and pipeline drugs

Competitive Landscape:

This report also provides a detailed analysis of the current obesity marketed drugs and late-stage pipeline drugs.

In-Market Drugs

- Drug Overview

- Mechanism of Action

- Regulatory Status

- Clinical Trial Results

- Drug Uptake and Market Performance

Late-Stage Pipeline Drugs

- Drug Overview

- Mechanism of Action

- Regulatory Status

- Clinical Trial Results

- Drug Uptake and Market Performance

| Drugs | Company Name |

|---|---|

| Wegovy (Semaglutide) | Novo Nordisk |

| Zepbound (Tirzepatide) | Eli Lilly and Company |

| Saxenda (Liraglutide) | Novo Nordisk |

| Qsymia (Phentermine/topiramate) | VIVUS |

| Contrave (Bupropion/naltrexone) | Currax Pharma |

| Xenical (Orlistat) | Roche / GlaxoSmithKline (as Alli) |

| Retatrutide (LY3437943) | Eli Lilly and Company |

| MariTide (Maridebart cafraglutide/AMG 133) | Amgen |

| Orforglipron (LY3502970) | Eli Lilly and Company |

| Survodutide (BI 456906) | Boehringer Ingelheim / Zealand Pharma |

*Kindly note that the drugs in the above table only represent a partial list of marketed/pipeline drugs, and the complete list has been provided in the report.

Key Questions Answered in this Report:

Market Insights

- How has the obesity market performed so far and how will it perform in the coming years?

- What are the markets shares of various therapeutic segments in 2024 and how are they expected to perform till 2035?

- What was the country-wise size of the obesity market across the seven major markets in 2024 and what will it look like in 2035?

- What is the growth rate of the obesity market across the seven major markets and what will be the expected growth over the next ten years?

- What are the key unmet needs in the market?

Epidemiology Insights

- What is the number of prevalent cases (2019-2035) of obesity across the seven major markets?

- What is the number of prevalent cases (2019-2035) of obesity by age across the seven major markets?

- What is the number of prevalent cases (2019-2035) of obesity by gender across the seven major markets?

- How many patients are diagnosed (2019-2035) with obesity across the seven major markets?

- What is the size of the obesity patient pool (2019-2024) across the seven major markets?

- What would be the forecasted patient pool (2025-2035) across the seven major markets?

- What are the key factors driving the epidemiological trend of obesity?

- What will be the growth rate of patients across the seven major markets?

Obesity: Current Treatment Scenario, Marketed Drugs and Emerging Therapies

- What are the current marketed drugs and what are their market performance?

- What are the key pipeline drugs and how are they expected to perform in the coming years?

- How safe are the current marketed drugs and what are their efficacies?

- How safe are the late-stage pipeline drugs and what are their efficacies?

- What are the current treatment guidelines for obesity drugs across the seven major markets?

- Who are the key companies in the market and what are their market shares?

- What are the key mergers and acquisitions, licensing activities, collaborations, etc. related to the obesity market?

- What are the key regulatory events related to the obesity market?

- What is the structure of clinical trial landscape by status related to the obesity market?

- What is the structure of clinical trial landscape by phase related to the obesity market?

- What is the structure of clinical trial landscape by route of administration related to the obesity market?